The Biden administration has finalized a new income-driven repayment plan known as SAVE, which will forgive some student loan borrowers’ balances after between 10 and 25 years of payments.

But federal Parent PLUS loans, which parents can use to help pay for their children’s undergraduate education expenses, cannot be paid off with SAVE plans.

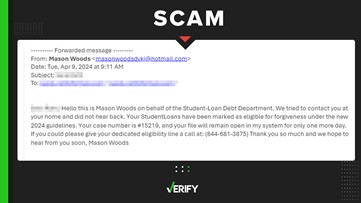

Terry asked VERIFY if there are other loan forgiveness options available to Parent PLUS borrowers.

THE QUESTION

Can Parent PLUS loans qualify for forgiveness?

THE SOURCES

- The U.S. Department of Education

- Consumer Financial Protection Bureau (CFPB)

- Finaid

- The Institute of Student Loan Advisors (TISLA)

- Student Loan Planner

- Abby Shafroth, director of the National Consumer Law Center (NCLC) Student Loan Borrower Assistance Project

THE ANSWER

Yes, federal Parent PLUS loans can qualify for forgiveness if they are consolidated. These borrowers must enroll in an income-contingent repayment plan or pursue public service loan forgiveness.

WHAT WE FOUND

Parent PLUS borrowers can have their remaining debt forgiven after certain periods of time if they enroll in a specific income-driven repayment plan or pursue public service loan forgiveness.

These forgiveness options are not related to the Biden administration’s student debt relief plan that was shot down by the Supreme Court.

Both options require Parent PLUS borrowers to consolidate their loans beforehand. Any federal education loan can be consolidated, even if you only took out one loan, according to Finaid.

Parents can apply for direct loan consolidation on the Department of Education’s studentaid.gov website.

Here’s a breakdown of the loan forgiveness options available to Parent PLUS borrowers.

Income-driven repayment

Income-driven repayment plans can lower your monthly student loan payments based on your income and family size, and eventually forgive your remaining loan balance.

The federal government offers four income-driven repayment plans, including the SAVE plan, but only one is available to parent PLUS borrowers who consolidate their loans. That plan is called an income-contingent repayment (ICR) plan.

If Parent PLUS borrowers on ICR plans still have debt after making payments for 25 years, their remaining loan balance will be forgiven, according to the Education Department.

ICR plans cap monthly payments at 20% of your discretionary income or offer fixed payments based on a 12-year loan term, whichever is lower. Discretionary income refers to the difference between your income and an amount the Education Department determines you must have to meet your basic needs.

The Consumer Financial Protection Bureau (CFPB) says the minimum payment for borrowers on ICR plans is $5.

Parent PLUS borrowers who have consolidated their loans can apply for an ICR plan on the studentaid.gov website.

Public Service Loan Forgiveness (PSLF) program

Parent PLUS borrowers who work full-time in qualifying public service jobs are eligible for full loan forgiveness after making 10 years’ worth of payments (totaling 120 payments).

Parent PLUS loans are only eligible for the Public Service Loan Forgiveness (PSLF) program if they have been consolidated into a direct loan and are being repaid under an ICR plan, the Education Department says.

Borrowers qualify for the PSLF program if they have worked full-time for a federal, state, tribal or local government, the military or a qualifying nonprofit. The Education Department has a tool to search for qualifying employers on its website.

Under PSLF program rules, only qualifying payments that borrowers make on their new consolidated loans can be counted toward the 120 payments required for loan forgiveness. Any payments that parents made on their loans before consolidating them will not count toward this forgiveness.

Double consolidation ‘loophole’

Two student loan advisory services, the Institute of Student Loan Advisors (TISLA) and Student Loan Planner, outline a double consolidation “loophole” that can allow Parent PLUS borrowers to access other income-driven repayment plans such as SAVE.

While some borrowers have had success with this process, it is “more complicated and the [Department of Education] has said it will prevent borrowers who consolidate after July 1, 2025 from using that approach,” Abby Shafroth, a student loan expert with the National Consumer Law Center, told VERIFY.