The Supreme Court ruled on June 30 that President Joe Biden’s administration overstepped its authority in trying to implement a one-time student debt relief plan.

Biden’s plan would have forgiven between $10,000 and $20,000 of federal student loan debt for people with annual incomes of less than $125,000 for individual borrowers and less than $250,000 for households.

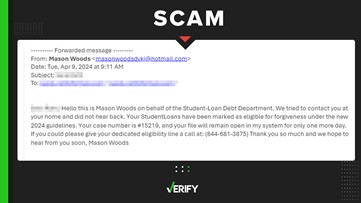

VERIFY is breaking down what borrowers need to know after the Supreme Court’s decision, including when payments will restart and if the Biden administration is looking into other options for debt relief.

THE SOURCES

- U.S. Department of Education

- Fiscal Responsibility Act of 2023

- Majority opinion in Biden v. Nebraska

- The White House

- Andrew Lautz, director of federal policy at the National Taxpayers Union Foundation

- Nicholas Creel, assistant professor of business law and constitutional law expert at Georgia College and State University

WHAT WE FOUND

When will student loan payments restart?

Student loan interest will start accruing on Sept. 1, 2023 and payments will be due starting in October, according to the Department of Education’s website. The department says it will “notify borrowers well before payments restart.”

This is because of the debt ceiling deal, which Biden signed into law in early June. It set an end date for the payment pause on federal student loans that began on March 13, 2020, requiring them to resume 60 days after June 30.

Federal student loan borrowers have not been required to make monthly payments since March 2020 and their loans have not accrued interest during the pause.

More from VERIFY: Yes, the debt ceiling deal requires student loan payments to restart

Though the pause is set to end soon, some borrowers who are unable to make payments on their loans will not immediately be penalized.

The Department of Education is instituting a 12-month “on-ramp” to repayment from Oct. 1, 2023 to Sept. 30, 2024, the White House said. That means “financially vulnerable borrowers” who miss monthly payments during this time will not be considered delinquent, reported to credit bureaus, placed in default or referred to debt collection agencies.

"Borrowers who can pay should do so, but this on-ramp period gives borrowers who cannot make payments right away the necessary time to adjust, enabling them to ultimately make their monthly payments and meet their financial obligations on their loans,” the White House said.

Is the Biden administration pursuing other options for student debt relief?

Following the Supreme Court’s decision, the Biden administration announced that it is taking steps “aimed at providing debt relief for as many borrowers as possible, as fast as possible, and supporting student loan borrowers.”

Secretary of Education Miguel Cardona has “initiated a rulemaking process” aimed at opening another path to student debt relief under the Higher Education Act, the White House said. It’s unclear what the potential student loan forgiveness plan would entail.

Cardona said in a tweet that his department is “using every tool available to provide the needed relief.”

The Department of Education issued a notice that announces a virtual public hearing on July 18 and asks for written comments from stakeholders on topics to consider in the alternative path to student debt relief. After the hearing, the department expects to begin “negotiated rulemaking” sessions in the fall.

Is there a new income-driven repayment plan for borrowers?

As part of the Biden administration’s response to the Supreme Court decision, the White House also announced that it finalized the Saving on a Valuable Education (SAVE) plan.

All borrowers will be eligible to enroll in this income-driven repayment plan later this summer before any monthly payments are due. Borrowers who sign up or are already signed up for the current Revised Pay as You Earn (REPAYE) plan will be automatically enrolled in SAVE once it is implemented, according to the White House.

The new SAVE plan will:

Decrease the amount that undergraduate loan borrowers have to pay each month from 10% to 5% of discretionary income.

Raise the amount of income that is considered non-discretionary and protected from repayment, guaranteeing that no borrower earning about the annual equivalent of a $15 minimum wage will have to make a monthly payment.

Forgive loan balances after 10 years of payments, instead of 20 years, for borrowers with original loan balances of $12,000 or less.

Not charge borrowers with unpaid monthly interest, so no borrower’s loan balance will grow as long as they make their monthly payments.

Do borrowers have other options to suspend student loan payments?

Student loan borrowers who are in a “short-term financial bind” may qualify for deferment or forbearance, the Department of Education says. Both of these options allow borrowers to temporarily suspend their payments.

However, loan interest will typically still accrue while your loan is in deferment or forbearance – you just won’t be penalized for failing to make payments. This means your balance will increase and you will end up paying more over the life of your loan.

Are there any other federal student loan forgiveness programs?

A number of other student loan forgiveness programs that have existed for years remain in place after the Supreme Court ruling. However, only borrowers who meet specific conditions qualify for them.

One program is Public Service Loan Forgiveness (PSLF), which forgives a borrower’s Direct Loans if they work in certain public service jobs and make 120 payments on their loans. The Department of Education says it has approved $42 billion for 615,000 borrowers in PSLF since Oct. 2021.

Any borrower with an IDR plan will have their remaining loans forgiven after making 20 to 25 years of payments. Whether you have balance left over to forgive depends on how large your income is relative to your debt, the Education Department says.

The Education Department also regularly eliminates student loan debt for borrowers who have been misled or suffered from misconduct by certain colleges in a program called borrower defense. These are usually for students who attended defunct for-profit colleges, such as ITT Technical Institute.

Other forgiveness programs listed by the Education Department’s Federal Student Aid website include forgiveness programs for teachers, people with disabilities, people who have died and people who have filed for bankruptcy.

More from VERIFY: No, Supreme Court ruling does not eliminate other student loan forgiveness programs

How does student debt relief differ from Paycheck Protection Program (PPP) loan forgiveness?

Some people, including U.S. lawmakers, have compared proposed student debt relief to Paycheck Protection Program (PPP) loan forgiveness.

The PPP, aimed at helping businesses keep their workers employed during the COVID-19 pandemic, offered loans worth up to $10 million to most small businesses, individuals and nonprofit organizations with fewer than 500 employees through May 2021.

The Pandemic Response Accountability Committee (PRAC), which tracks how pandemic relief funds are used, said in its October 2022 update that the average amount of PPP loan forgiveness was $72,100 – over $50,000 more than the maximum amount of Biden’s proposed student loan forgiveness.

But student debt relief and PPP loan forgiveness is “not quite an apples to apples comparison,” Andrew Lautz, director of federal policy at the National Taxpayers Union Foundation, told VERIFY.

While Congress created the PPP and its accompanying loan forgiveness through federal law, the Biden administration tried to use other methods for student debt relief.

“The law that President Biden is using is not as overtly clear as when these types of mass forgiveness programs can be done,” Nicholas Creel, a constitutional law expert at Georgia College and State University, said.

VERIFY digital journalist Emery Winter contributed to this report.