Banks and credit unions have been getting pushback for their long-standing use of overdraft fees, or penalties for covering a purchase when a customer doesn’t have enough funds in their account.

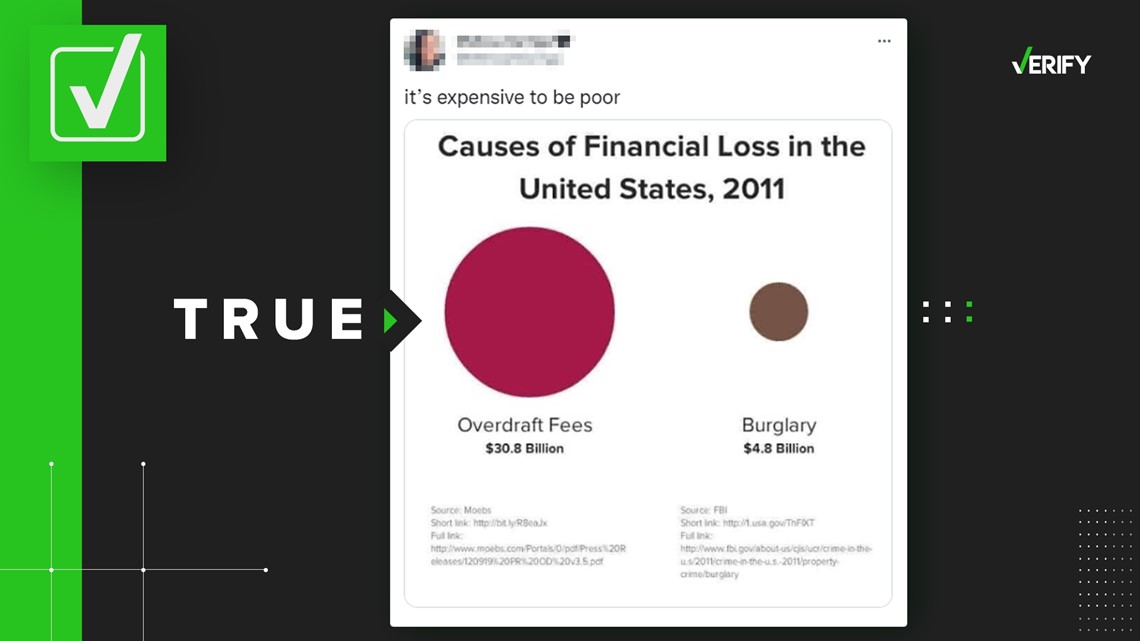

A user on Twitter wrote “it’s expensive to be poor,” alongside a meme that compared financial losses incurred by Americans in 2011 from both overdraft fees and burglary. The graphic claims the cost of burglary totaled $4.8 billion, while overdraft fees accounted for $30.8 billion in losses, a difference of more than six-fold. The post has been shared more than 14,000 times. Another post references the same numbers.

THE QUESTION

Did overdraft fees cost Americans more than six times as much as burglaries in 2011?

THE SOURCES

- Consumer Financial Protection Bureau

- FBI

- Moebs Services

- Bruce McClary, Senior Vice President, Membership & Communications, National Foundation for Credit Counseling (NFCC)

- Federal Deposit Insurance Corporation (FDIC)

THE ANSWER

Yes, overdraft fees cost Americans more than six times as much as burglaries in 2011.

WHAT WE FOUND

The meme’s data correctly shows overdraft fees cost Americans more than six times as much as burglaries in 2011, a difference that nearly doubled by 2019, VERIFY confirmed.

VERIFY checked the sources listed at the bottom of the graphic: An economic research group called Moebs Services that studies overdraft fees, and FBI crime data.

The meme’s first statistic, which cites Moebs Services, says Americans paid $30.8 billion in overdraft fees in 2011. That report did indeed find banks and credit unions took in $30.8 billion in overdraft revenue during the fiscal year ending in June 2011. Moebs’ data was later cited in a 2013 report on overdraft fees published by the Consumer Financial Protection Bureau.

The second data point cited in the viral meme is from the FBI. The tweet claims victims of burglary, or the “the unlawful entry of a structure to commit a felony or theft,” as defined by the FBI, lost $4.8 billion in 2011. That’s true; the bureau's data from 2011 reports the same amount was lost in burglaries that year.

Burglaries differ from robberies and larcenies, which do not involve illegal entry into a home or building. The FBI estimates Americans lost an additional $6.4 billion to robberies and "larceny-theft" crimes in 2011.

Though the FBI has reported declines in burglary losses since 2011, banks’ revenue from overdraft fees has largely remained consistent. Moebs Services reported overdraft fees totaled $31.3 billion in 2020 and $32 billion in 2021.

Overdraft protection is not automatically the default for all bank accounts. Customers legally must opt-in in order for their bank to provide this service, which was originally “created in the spirit of convenience” when checks were mailed, according to the Consumer Financial Protection Bureau.

But the CFPB also says financial institutions have become too reliant on overdraft penalties and similar non-sufficient funds fees (NSF), or charges for bounced transactions.

Since 2015, the agency has taken legal action against multiple financial institutions for deceptive or fraudulent overdraft practices and marketing and collected data on how these fees affect consumers. In 2021, CFPB Director Rohit Chopra announced the organization would pay close attention to banks that rely heavily on overdraft fees.

“Over time…banks figured out how to make even more money off depositors for the ‘privilege’ of holding their money. Rather than compete on the highest interest rate to attract customers, our nation’s largest banks now provide hardly any interest on deposits and charge billions in fees,” CFPB Director Rohit Chopra said in an announcement about the initiative.

On April 6, attorneys general in 15 states plus D.C. urged JPMorgan Chase, Bank of America, U.S. Bank and Wells Fargo to eliminate overdraft fees, citing the charges’ disproportionate effect on people of color and low-income customers.

Some banks have already made changes. In January, Bank of America announced it would eliminate and reduce some fees related to low account balances. Citi announced in February it would cut overdraft fees altogether, following similar moves from Capital One and Ally in 2021.

But many experts say too many vulnerable customers are still falling prey to these fees. Critics say the charges, typically around $35, often push cash-strapped customers further into debt.

Some banks will continue to charge for every day the account remains in the negative, according to the Federal Deposit Insurance Corporation (FDIC.) Without money to pay off negative balances, charges can snowball.

CFPB data shows less than 9% of bank customers pay 10 or more overdrafts per year, making up close to 80% of all overdraft revenue. Frequent overdrafters are also more likely to have a lower credit score, implying their access to credit cards is limited, the CFPB also concluded in a 2017 report.

“These overdraft fees are the same dollar amount for somebody making minimum wage as they are for somebody making a hundred thousand dollars a year. It is hitting people hard, especially those who are struggling the most right now,” said Bruce McClary, senior vice president for Membership & Communications at the National Foundation for Credit Counseling (NFCC.)

Avoiding these fees can also be confusing when juggling low balances. It’s not always clear when recently-deposited funds will be available to cover pending charges, or when purchases will post to an account.

“Many large banks today penalize their own customers based on things outside their control like the difference between authorization and settlement, the significance of the timing gap between the two, the amount of time a credit may take to show up in the account, the use of one kind of balance over another for fee calculation purposes, or the order of transaction processing across different types of credit and debits,” Chopra said in 2021.

To avoid uncertainty, McClary recommends reading the fine print to understand the most cost-effective way to avoid fees. He also suggested setting up automated alerts that will send notifications when an account's balance is low.

The CFPB also suggests doing the following:

- Keep track of automatic payments

- Opt out of overdraft coverage. If you don't have enough money in your account to cover a purchase or withdrawal, your card will be declined but you won't incur an overdraft fee.

- Link to a savings account. If your checking account can't cover a charge, some banks will allow you to set up automatic transfers from a savings account. You may still be charged a fee for this service but it's usually lower than overdraft protection. This can also be done with a credit card or line of credit, but you'll owe interest on the amount borrowed. Do the math to see which option is most cost-effective.